In this article we discuss the Personal Allowance Taper & Annual Allowance Taper – what you should be aware of and how to mitigate the impact.

As is customary, from time to time, governments introduce new measures to increase the tax intake. From a tax on Candles in the 1780’s, the Window tax of the 1690’s, to an interesting tax on Beards in 18th century Russia.

In the last 10 years successive UK governments have introduced some slightly more subtle changes to increase tax receipts. Two of these lesser known changes were introduced in 2016 – the Personal Allowance Taper and the Annual Allowance Taper, which primarily affect those with high earnings. How does it affect you and what can you do about it?

“An estimated 250,000 people in the UK may be affected by the Personal Allowance Taper…”

Personal Allowance Taper: What is it? What effect does it have?

Your Personal Allowance is the amount of income that you can earn tax free. It currently stands at £12,500 per annum for 2019/20. In April 2016, the government introduced the Tapered Annual Allowance which affects people who earn above £100,000.

At this level, individuals will start to lose their personal allowance at a rate of £1 above the threshold. Therefore, if you earn £125,000 or more, your Personal Allowance will be reduced to zero. This results in an effective marginal rate of income tax for earnings between £100,000 – £125,000 of 61% in Scotland. This is because in addition to paying higher rate tax of 41% on any income above £100,000, there is the impact of losing some or all of the personal allowance and paying 41% tax on that too.

What can I do about this?

Thankfully with careful planning, you may be able to lessen the impact, although much depends on your personal circumstances.

One way that you may be able to gain back your tapered personal allowance is by making pension contributions – either personally or through salary sacrifice (you should note that employer contributions cannot be used to regain the personal allowance). Again, this is dependent on your personal circumstances and careful planning is required.

If you would like a no-obligation appraisal of your current circumstances, please get in touch and make an appointment. -> Contact Us

Annual Allowance Tapering for High Earners:

The annual allowance is the amount of tax relievable pension contributions you can make each year. This includes any contributions paid by you, on your behalf by your employer or any other 3rd party.

The allowance is currently £40,000, within which, gross contributions are restricted to the higher of £3,600 or 100% of relevant UK earnings. The annual allowance applies to both defined benefit (final salary) accrual as well as payments made into a defined contribution pension in each pension input period.

What is the Tapered Annual Allowance?

The Tapered Annual Allowance was introduced by the government in 2016, in an effort to limit the cost of pensions tax relief. It may apply to all pension savings made by you (or on your behalf); and depending on your level of taxable income within the tax year, it may result in a reduction of your annual allowance.

This applies to individuals with a “threshold income” of over £110,000 and an “adjusted income” of over £150,000.

How the taper works:

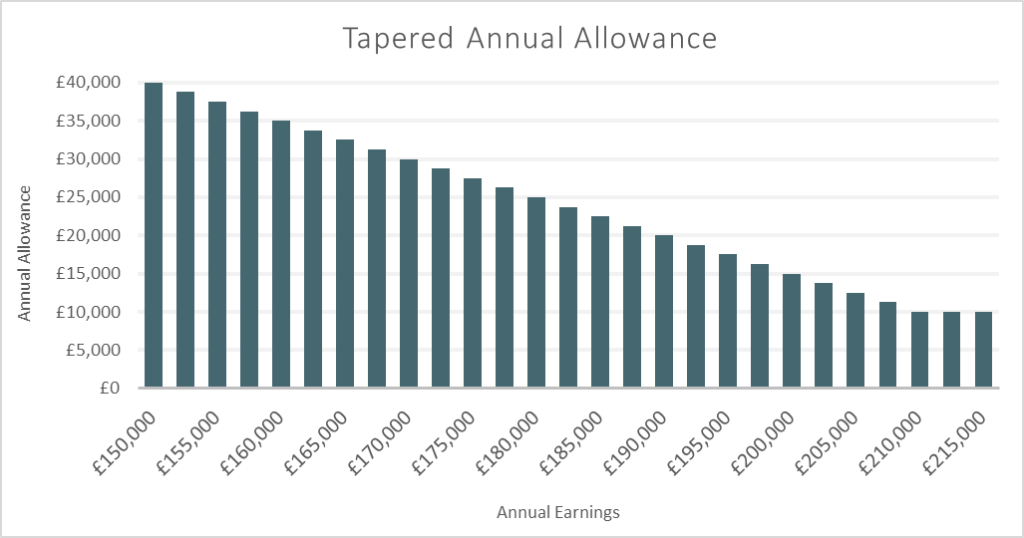

If both the adjusted income and threshold income tests are breached, the annual allowance is reduced by £1 for every £2 over the “adjusted income” figure. The maximum reduction is £30,000, therefore, for anyone with income of £210,000 or more the annual allowance will be £10,000 (as per table below).

How is this calculated:

The limit for the adjusted income is £150,000 and is defined as total taxable earnings plus any employer contributions paid on your behalf, less any taxed lump sum death benefit received. If this is breached, a second test against the threshold income is undertaken, which is your total taxable income, plus any salary sacrifice arrangements since 9th July 2015, less any relevant personal pension contributions and lump sum death benefits. The limit for the threshold income is £110,000. Tapering only applies if both the adjusted income and the threshold income are breached.

What can I do about this?

The calculations and planning around Annual Allowance and the Tapered Annual Allowance can become fairly involved, particularly when individuals remain active members of defined benefit (nee final salary) pension schemes and where transitional pension input periods can muddy the waters.

As such, the proper advice can add tangible value. If you would like a confidential, no-obligation appraisal of your current circumstances, please get in touch and make an appointment.

This post is for information purposes only and is certainly no substitute for regulated, independent financial advice. The value of an investment and the income derived from it may fall as well as rise. Returns are not guaranteed and you may get back less than you originally invested. The Financial Conduct Authority do not regulate some forms of tax advice. The information in this post is subject to our understanding of current and – in some cases – expected legislation which may be subject to change in the future.

Further Reading: https://www.gov.uk/guidance/pension-schemes-work-out-your-tapered-annual-allowance