Independent Mortgage Advice

Finding the right mortgage for you…

A mortgage is the largest financial commitment that many of us will ever make. And so, it is important to find the right mortgage for your home

There are over 200 mortgage lenders in the UK, including the main high street banks such as Lloyds, RBS, Barclays and Santander.

Although it’ll come as little surprise that the largest banks will often not offer the lowest rates. We are Independent advisers which means that we search the whole of the market, accessing the best rates and ensuring you have the best mortgage available.

We provide free mortgage consultations – which help answer some of the most common questions that first time buyers or those looking to remortgage have. For example: How much can I borrow? How much can I afford? What are the best mortgage rates available?

Remortgaging your home

It is sensible to review your mortgage from time to time, and consider switching if you find a better, more suitable deal. With over 200 mortgage lenders in the UK, you may be able to access a deal with a better interest rate. As we are independent advisers, we can look across the whole of the market and identify the most suitable mortgage for you.

Why remortgage?

There are two main reasons that people look to remortgage.

1. To get a better interest rate

Perhaps the most common reason that people look to remortgage is to access a better interest rate and reduce their monthly payment. Most often, this will be when your current mortgage deal is due to end – or has already ended.

Many lenders offer an introductory period – often for the first 2,3 or 5 years. Once this initial period is over, they would normally move you onto their Standard Variable Rate. This often results in your monthly mortgage payments increasing/ becoming more expensive.

“up to 44% of the UK’s 10.8 million mortgages are likely to be on their provider’s Standard Variable Rate, which can be more than double the interest rate of their original introductory offer.”

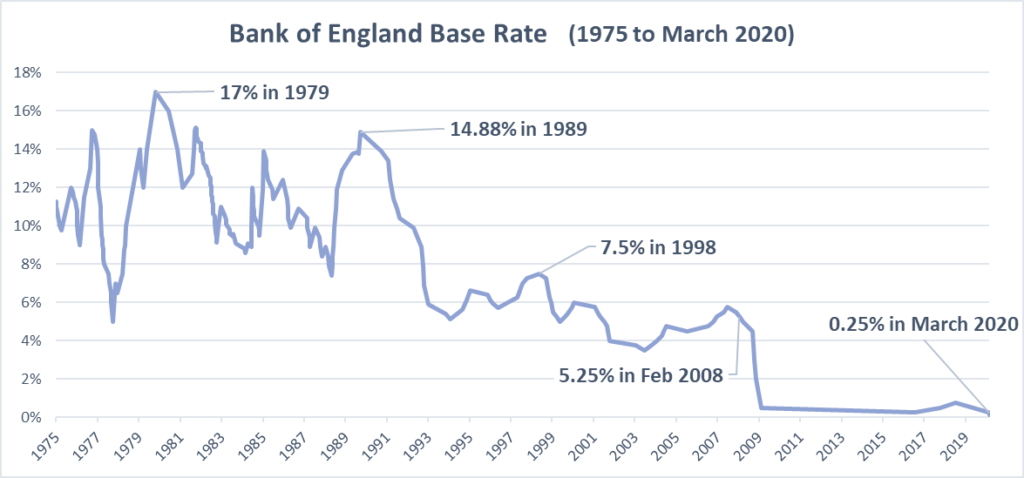

With two rate cuts in the first half of 2020, the Bank of England base rate is at historic lows (as shown in the graph below). In theory, this is good news for borrowers, as it should likely reduce mortgage interest rates.

However, this may not be the case for all borrowers on a Standard Variable Rate. This is because the Standard Variable Rate that mortgage lenders set is at their own discretion and so they are not obliged to pass on any rate cuts to borrowers. In practice, this means that if you are on a Standard Variable Rate, then you may be paying a significant amount more each month than you would be if you were on e.g. a Fixed Rate deal.

According to recent analysis carried out by Experian, “up to 44% of the UK’s 10.8 million mortgages are likely to be on their provider’s Standard Variable Rate, which can be more than double the interest rate of their original introductory offer.” – www.experianplc.com/media/news/2020/millions-of-mortgage-holders-could-save-more-than-5000/

2. Remortgaging for more flexibility

One feature that many look for is the flexibility to overpay their mortgage from time to time. This allows you to reduce your mortgage loan more quickly. Not all mortgages deals allow overpayments – and with some lenders you would incur a penalty for overpaying your mortgage.

Offset mortgages can be very effective in certain circumstances. It can allow you to use savings you have to reduce the amount of interest that you pay; also giving you the option to access those savings if or when you need to. For more information on Offset Mortgages, see the article: Power of an offset mortgage.

Buying your new home

Buying a new home can be both a stressful and exciting time. You will likely be making several important decisions that will shape and impact you and your family for some years. Finding the right mortgage and having comfort that you have the best possible mortgage deal for you, is clearly important.

Seeking independent, whole of market mortgage advice can help give you confidence that you have found the best possible mortgage for you on the market.

First-time buyers

For those looking to get onto the property ladder and buy their first home, it can be difficult to know where to start. How much can you borrow? How much deposit do you need? What will your monthly payment be? At Glasgow Wealth, we are able to help guide you through the process and give you peace of mind.

How much can I borrow?

It was once a simple multiple of earnings; however, this has since changed and the amount you can now borrow is based largely on affordability; the amount the lender deems you can afford to repay each month combined with your credit rating.

Servicing debt such as credit cards or car loans will reduce your level of borrowing, as will other properties you own and the number of dependent children living at home. The calculator below will help give you a broad idea of what you may be able to borrow; although an affordability calculator would give a better indication of what mortgage providers would be willing to lend to you. Contact us for more information or to book a free mortgage consultation.

For more information or for a more accurate idea of how much you may be able to borrow and which mortgages may be available, get in contact to arrange a free consultation.

Repayment Options

A mortgage is made up of two components. Firstly the Capital: which is the money that you borrow. Secondly, is the Interest: which is the charge made by the lender for the amount that you borrow.

There are two ways to repay the loan:

- Capital Repayment: This is where you pay back the loan plus the interest and at the end of the term the full loan has been repaid and there is nothing more to pay

- Interest Only: This is where you only pay the interest to the lender with the capital balance remaining outstanding at the end of the term. You will need to arrange a method of repaying the loan (e.g. ISA or tax-free cash from a pension plan) and if you are unable to do so, options such as re-mortgaging or selling the property should be explored.

The Different Types of Mortgage

Many mortgage products have flooded the market over time however, the main types are as follows:

-

- Variable rate mortgages

What you pay each month can change at any time so your payments could go up or down – this is often linked to the movement in the Bank of England (BoE) base rate.

- Tracker mortgage

Is a variable rate mortgage where there is an automatic link built in, so interest tracks an index, usually the bank base rate

- Discounted

A variable rate loan with the interest rate set a specified percentage rate below the standard variable rate for a fixed initial period

- Offset Mortgage

This works by linking a savings account to your mortgage so you only pay interest on the balance. If you borrow £100,000 and have £10,000 in the linked savings account, then your interest repayments are based on £90,000. An offset mortgage can be very effective for many – as outlined in our article: The power of an offset mortgage.

- Fixed rate mortgage

The interest rate or the amount you pay every month is fixed at the outset and will stay the same throughout the duration of the deal regardless of changes in interest rates.

- Capped and/or collared

Capped rates are guaranteed not to rise above a certain percentage rate for a fixed period. They can also be collared; the rate will not fall below a certain interest rate. The two can be applied together, so rates are guaranteed to be between an upper and lower limit for a specific period.

- Variable rate mortgages

If unsure which type of mortgage would be best for you, then contact us to speak to a mortgage adviser for a free consultation.

YOUR HOME IS AT RISK IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR OTHER LOAN SECURED ON IT .

REDEMPTION PENALTIES MAY BE PAYABLE ON THE EARLY REDEMPTION OF A MORTGAGE LOAN

Below is a brief explanation of some more common terms that are used when looking at mortgages.

Term

The deal period is not to be confused with the term. The term of the mortgage is the duration between receiving funds from a lender and the date when the loan is to be repaid. The term can run up to 35 years and beyond however, some lenders will not lend beyond a certain age, say 75.

Early Repayment

Should you wish to terminate your mortgage within the deal period or pay more than the agreed repayments, you are likely to face charges for doing so. Every lender is different so please check before making over payments.

Higher Lending Charge

A charge made by the lender when the loan to value exceeds a specified threshold (often 75%). It is an insurance to cover the risk of proceeds of a forced sale being less than the mortgage loan.

Land & Building Transaction Tax (LBTT) Calculator

YOUR HOME IS AT RISK IF YOU DO NOT KEEP UP REPAYMENTS ON A MORTGAGE OR OTHER LOAN SECURED ON IT .

REDEMPTION PENALTIES MAY BE PAYABLE ON THE EARLY REDEMPTION OF A MORTGAGE LOAN